I’m Isaac Saul, and this is Tangle: an independent, nonpartisan, subscriber-supported politics newsletter that summarizes the best arguments from across the political spectrum on the news of the day — then “my take.”

Are you new here? Get free emails to your inbox daily. Would you rather listen? You can find our podcast here.

Today's read: 11 minutes.

From our advertiser: Count me as one of over 4 million people who start their day by reading Morning Brew — the free daily email covering the latest news across business, finance, and tech. Morning Brew is a great complement to Tangle if you're looking to cover your bases outside of politics, and it's my go-to for all things business and finance. Recent headlines:

- The market is hangry right now: How Deutsche Bank is different than Credit Suisse

- TikTokers rally around CEO after viral hearing.

- Chicago man takes the debate over boneless wings to court. (Hey, it’s not all tech and business).

The best part? It’s free and only takes 5 minutes to read so that you can get all of the most relevant updates and move on with your day. Sign up for free here.

Friday's clickbait.

In place of today's reader question, I'm going to follow up on the (very controversial) Friday edition we published. That story, along with the results of the newsletter, come after today's main topic.

Quick hits.

- First Citizens Bank agreed to purchase $72 billion of Silicon Valley Bank's assets, while another $90 billion will stay in FDIC receivership. (The purchase)

- At least 26 people were killed and dozens more injured when 12 tornadoes touched down in Mississippi and Alabama over the weekend. (The tornados)

- Israeli Prime Minister Benjamin Netanyahu fired his defense minister Sunday after the minister publicly criticized his judicial reforms, setting off another wave of widespread protests across Israel. (The protests)

- Russia’s President Vladimir Putin said Russia will station tactical nuclear weapons in Belarus, though there is no evidence yet it has moved the weapons. (The comments)

- The Los Angeles Unified School District has struck a deal with school employees to end a strike in the country's second largest school district. (The deal)

Today's topic.

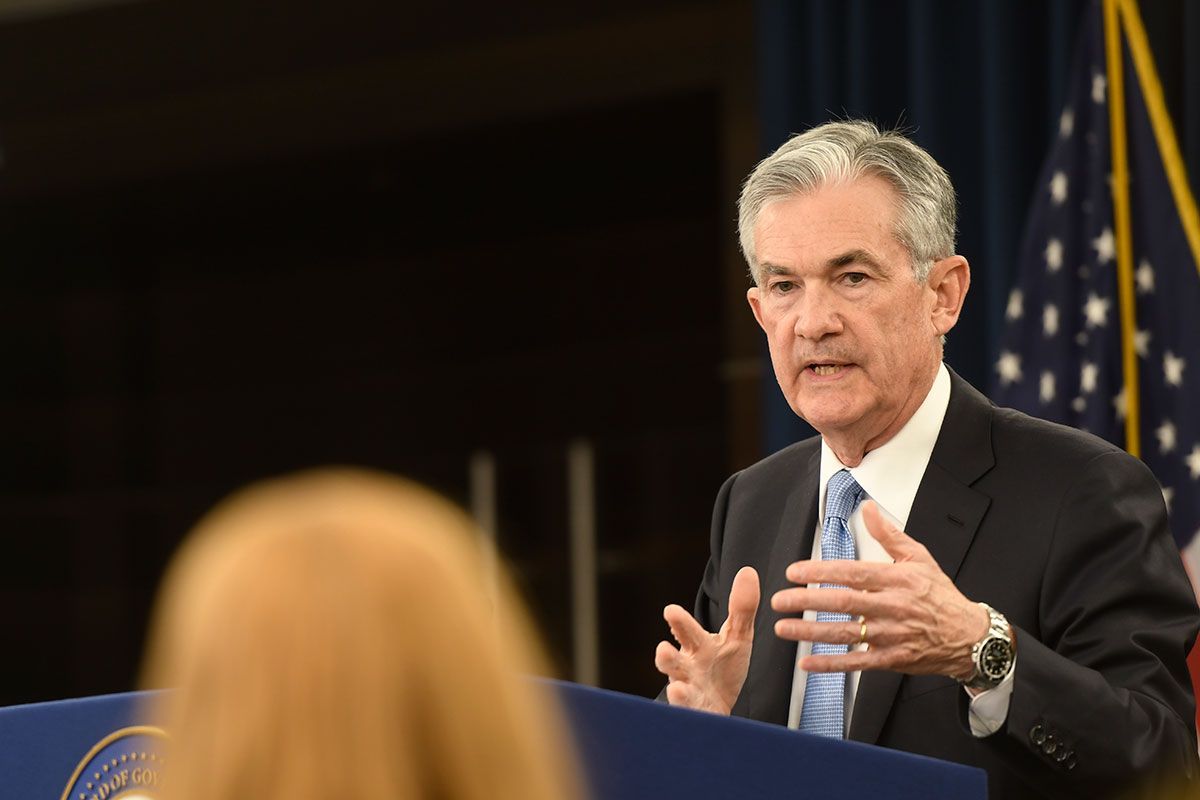

The Fed’s rate hike. Last week, the Federal Reserve raised interest rates for the ninth time since March of 2022, this time by a quarter of a percentage point. Interest rates are now at 5%, the highest level since 2007. The move comes at a time of unusual uncertainty, as some bankers and investors urge the Fed to pause the rate increases because of the failure of several mid-sized banks. The Fed expressed caution about the banking crisis and also indicated rate hikes may be nearing an end, despite the persistence of inflation.

Reminder: Interest rates represent the cost for banks to borrow from the Federal Reserve. When the Fed raises interest rates, that increase is passed through to things like credit card debt, mortgages and loans. The Fed uses interest rate hikes to slow spending and investment in order to tamp down inflation, and has been raising interest rates to battle inflation for a year.

Meanwhile, inflation is measured by the Consumer Price Index (CPI), which is designed by the Bureau of Labor Statistics to measure price fluctuations for urban buyers, who represent the vast majority of Americans. The CPI tracks 80,000 items in a fixed basket of goods and services, representing everything from gasoline to apples to the cost of a doctor's visit.

There were some questions about whether The Fed would or should hike interest rates again. The failure of Silicon Valley Bank (SVB) was, in part, precipitated by increased interest rates which devalued government bonds the bank owned. Before SVB's failure, the Fed was expected to raise interest rates by half a percentage point, but was then put in the difficult and unusual position of having to decide how to keep fighting inflation while also navigating a potential banking crisis.

Fed Chair Jerome Powell emphasized that the inflation fight isn't over yet. Historically, the Fed has aimed to keep inflation around 2% — but since October of 2021 it has consistently been around 6% on a year-over-year basis.

“The process of getting inflation back down to 2% has a long way to go and is likely to be bumpy,” he said in a post-meeting news conference.

Today, we're going to look at some commentary from the right and left about the rate hike and what the Fed should have done, then my take.

What the right is saying.

- Many on the right say the Fed is facing a crisis of its own making and urges it to focus on inflation.

- Some say the Fed should focus on its anti-inflation credibility.

- Others say Fed Chairman Jerome Powell must see the job through on rate increases despite the extraordinary outside pressure to ease up.

The Wall Street Journal editorial board said the Fed is trying to "thread the needle" on interest rates.

"If we're all lucky," the board said, Fed Chairman Jerome Powell will be right that "the American banking system is safe and he will get inflation under control." The hike was "less than the half-point increase markets had expected" and the rate-raising cycle "appears to be one more and done. That’s out of step with inflation that remains well above the Fed’s 2% target, and the central bank’s prediction that inflation will fall rapidly this year may be too optimistic given its poor forecasting record."

Two weeks ago, price data had "signaled higher inflation," but then came SVB's failure and other turmoil that "exposed the threats that rapidly rising rates pose to a financial system distorted by more than a decade of very loose monetary policy." Powell said the Fed views inflation and bank turmoil "as two separate challenges," which is "the right message to send markets to maintain anti-inflation credibility." But it's also risky. If the Fed fails to prevent a larger panic, it "could be forced to ease before it conquer[s] inflation," but both issues are "problems of the central bank's creation."

In National Review, Steve H. Hanke and Manuel Hinds called it a "self-directed tragedy."

"The Fed expanded the money supply at an unprecedented average annual growth rate of 19 percent between February 2020 and February 2022, and then reversed gears and began to shrink the money supply by an unprecedented cumulative 2.2 percent between March 2022 and January 2023," they wrote. "To put those numbers into context, based on the quantity theory of money, the rate of growth of the money supply that is consistent with the Federal Reserve’s hitting its 2 percent inflation target is 5–6 percent per year. These dramatic Fed maneuvers stressed the banking system, and SVB and other regional commercial banks are the collateral damage."

If that wasn't bad enough, "regulation of SVB falls under the purview" of the San Francisco Fed, where "any bank examiner" should have seen the writing on the wall. The Fed is now between a rock and a hard place. One option is "to engage in a monetary squeeze to fight inflation while inflicting pain on the commercial-banking system. The second option is to provide commercial banks with liquidity, which will probably set the Fed back in its fight against inflation."

In The Washington Examiner, Tiana Lowe asked "if this was Jerome Powell's Paul Volcker moment?"

"As the saying goes, the Federal Reserve usually raises interest rates until something breaks. After one year and 450 basis points of tightening, something has finally broken," Lowe wrote. Powell's resolve to keep fighting inflation "has persisted so far in a period when raising rates has been relatively easy." Now, he must prove if he is the man for the moment. "It is, or at least should be, easy to raise rates while the economy is still roaring. It is much harder to stomach the political pain and Wall Street wailing when raising rates after a financial break sparks investor panic."

Just like in 1984, when Volcker did the right thing, "Powell should not prioritize financial stability over his legal mandate to restore price stability." CPI inflation was 6% in February, "three times the Fed's inflation target," and Core PCE, "the Fed's preferred inflation measure, actually rose last month... Is it politically possible for Powell to pull this off? Not that Powell should care, but recall that President Ronald Reagan won 49 states during his 1984 reelection, in which Volcker had interest rates at 9% while inflation was 4%." If Powell wants to prove "the Fed stands independent," he will "see the job through."

What the left is saying.

- The left is split on the hike, with some saying Powell should have paused while others say mixed signals are more dangerous.

- Some argued pausing rate hikes with signals they would come back would have been the best decision.

- Others say inflation is the real and immediate threat, and should be the Fed's main focus.

Before the rate hike was announced, The Washington Post editorial board urged The Fed not to raise rates.

Despite the "stubborn" inflation problem, "there's a larger concern," the board said. "The rapid downfalls of Silicon Valley Bank and Signature Bank have zapped confidence in critical parts of the banking sector and triggered concerns about what is next to rupture. The Federal Reserve should temporarily pause interest rate hikes on Wednesday to give the financial system time to adjust to the new reality." Bank failures are scary and "people are shaken" all while "regional banks remain under pressure."

The Fed should "signal in its forecasts" that more hikes are coming, including "at the next meeting on May 3... But the Fed’s ultimate job is risk management, and right now the bigger risk is further harming financial stability." There are 190 banks at "similar" risk of a squeeze like the one at Silicon Valley Bank. "Regional banks are a big driver of commercial real estate," the board wrote. "Construction job openings were already falling fast in January, and this crisis could accelerate the retreat. The full extent of the fallout in numerous industries isn’t yet clear."

The Bloomberg editorial board said Powell's "balancing act" raises some questions.

The Fed "split the difference" between "the bigger increase it signaled earlier this month and the pause that many demanded" over the banking crisis. It's a "defensible compromise," but "cracks are showing in the central bank’s reasoning." At the moment, "entrenched inflation is the greater danger," and "interest rates should be set according to macroeconomic conditions." Powell maintained "the Fed loses nothing by moderating its anti-inflation strategy until it has a clearer view of where things are headed," and a small increase in rates with "the stress-induced tightening of financial institutions" will keep prices down.

It's a "plausible but flawed" logic. "The Fed can’t credibly promise to raise rates later if it’s too easily deflected by doubts about where things are heading," the board said. "The so-called ‘hawkish pause’ — timidity now, determination later — is a contradiction in terms. And the supposed tightening due to financial uncertainty is probably exaggerated... high inflation — the biggest problem the economy faces — is not a hypothetical issue: It’s here and now. If the Fed is suspected of flinching, it will become very much harder to solve."

In The Guardian, Robert Reich also called on the Fed to pause rate hikes "to prevent more bank runs."

Yes, "higher rates could imperil more banks, especially those that used depositors' money to purchase long-term bonds when interest rates were lower." But "the sensible thing would be for the Fed to pause rate hikes long enough to let the financial system calm down. Besides, inflation is receding, albeit slowly. So there’s no reason to risk more financial tumult." The Fed already "bailed out uninsured depositors at two banks and signaled it would bail out others."

One advantage of being a bank "is that you get bailed out when you make dumb bets." This is why central banks and bank regulators "must not only pause interest rate hikes" but also "join together to set stricter bank regulations" and ensure that instead of a race to the bottom, we have a "race to protect the public... If the public loses confidence in banks, the financial system can’t function."

My take.

Reminder: "My take" is a section where I give myself space to share my own personal opinion. If you have feedback, criticism, or compliments, don't unsubscribe. You can reply to this email and write in. If you're a subscriber, you can also leave a comment.

- I think Powell made the right call, and may have even gone too soft.

- Inflation should continue to be the Fed's number one priority.

- Not just that, but the banking crisis is already being addressed.

I think Powell made the right choice. If anything the "compromise" of only raising rates 0.25% is what was risky.

The complexities of our banking system are deep, and I'll be the first to concede that it's not my area of expertise. So I want to defer to the folks above who write specifically about these issues for a living.

Still, there is an obvious point here that I don't see a lot of people making. The Fed has been raising interest rates for months in an effort to fight inflation, and has committed to those hikes with the expectation it would cost hundreds of thousands of people their jobs and set off a potential recession. The banking crisis at SVB and the instability elsewhere was obviously caused in part by those hikes, which followed years of loose monetary policy.

But it was also caused by its own mismanagement, bad bets, and shoddy regulation. When we first covered the SVB failure, I wrote that depositors "did nothing wrong" but trust a bank. Writers like Matt Levine (and many knowledgeable Tangle readers) have successfully convinced me otherwise, arguing that many of these depositors were financially savvy, super-educated, well-funded start-up founders who could have known better but didn't really care.

The banking system already has regulations and oversight that are being leaned on, and the SVB failure showed that depositors are going to be looked after in the event of another bank failure. That alone should be enough to tamp down fears. Inflation is very real, very much here, and continues to threaten the U.S. economy as a whole.

As others have written above, the Fed's central job is price control, so it should prioritize crushing inflation. Given how much the government is already doing to stabilize the banks, I think pausing interest rate hikes would have been both redundant and much riskier in the long term. Powell seems to have made the right choice, though the 0.25% compromise hike seems a little like a wobble. It's hard to blame him for wanting to appease everyone and keep things calm during such an uncertain time, but writers like Tiana Lowe (under "What the right are saying") are right to emphasize that this can't be about sentiment or appeasement. It has to be simply about the data, which continue to show persistent inflation, and which Powell is singularly tasked with addressing.

Hopefully, the Fed’s focus remains there unless (or until) there is a real banking crisis to navigate.

Friday's clickbait...

Okay, first of all: I'm sorry for the scare. It quickly became apparent to me that a lot of readers opened Friday's email actually fearing something had happened to me or my family, or was going to happen to Tangle.

Given how personal this newsletter is for me, and the wonderful relationships I've built with so many readers in this community, I did not adequately think through how that subject line might hit everyone. I recognize a lot of people opened the email out of personal concern for me rather than some addiction to negative news. The experiment was probably a failure in the scientific sense.

Still... the results were basically what I expected. 67% of readers opened the email, which means it will probably be at 68% or 69% in a week, when folks who tend to read later go through and check their inboxes. It wasn't just the most opened email of the week, but it may end up being the most opened newsletter I've ever published. Recently, "We got a lot wrong about Trump and Russia" and "My response to your criticism" both got 65% open rates. Last week’s newsletter’s open rates were 61%, 59%, 56%, 58%, then Friday’s 67% (and counting).

The article also drove over 70 comments on the website, the most we've ever gotten on a Tangle piece. About 20 people became paying subscribers, around 50 donated to our tip jar, and about 70 people unsubscribed from the newsletter (presumably because they were mad about the clickbait!).

Also, the most clicked link in the story was the NBC News article on the contaminated eye drops, which got 537 clicks (1.3% of all readers who opened the email) even though I asked readers to try not to click it.

One thing is clear from the responses to this experiment: Despite being really tired of the non-stop negativity, people have a really hard time avoiding it. It’s worth it for all of us to consider how we can fight negativity bias in our own ways. I will keep this in mind as we continue to produce Tangle.

One reader wrote in and said, "My gut reaction after the first paragraph was irritation… but after reading it, you make an amazing point. This is a phenomenal Friday edition. Thanks Isaac."

Another said, "Using gross clickbait tactics to prove a point about gross clickbait tactics is still gross. Please don’t do this again."

One reader sent me an email with the subject line "You really suck!" which, of course, I immediately clicked. The body of the email was a nice note with gratitude about Tangle; so you all should know I immediately fell for my own trick.

A lot of people just wrote in to say something nice about how much Tangle means to them... which made me realize I forgot to mention one admittedly cliche point I should have included in the piece: Positivity, like negativity, is also very contagious. That alone is one of the best reasons to make an effort to focus more on the good.

I promise never to use fake clickbait again and, as is our policy, to refrain from using real clickbait in our newsletter. I appreciate you all writing in with your concern and kind words — the response to the piece really was overwhelmingly positive. If you missed the story, titled “Some very sad, terrible news to share,” you can read it here.

Under the radar.

Honduras announced it would establish diplomatic ties with China and formally cut ties with Taiwan, leaving the island nation with just 13 diplomatic allies. Most of those partners are small states in Central America and the Pacific, The Wall Street Journal reports. “Taiwan is an inalienable part of Chinese territory and as of this date, the Honduran Government has informed Taiwan about the severance of diplomatic relations, pledging not to have any official relationship or contact with Taiwan again,” the Honduran Foreign Ministry said. Honduras was weighing packages of aid from both Taiwan and China when it made the decision. The Wall Street Journal has the story (paywall).

Numbers.

- 186. The estimated number of banks that could face a similar fate as Silicon Valley Bank, according to one study.

- $3.44. The current average price of a gallon of gasoline in the United States.

- $4.24. The average price of a gallon of gasoline in the United States a year ago.

- 9%. The year-over-year rate of inflation in June, at its peak.

- 6%. The year-over-year rate of inflation this month.

- 9.5%. The percentage increase in food prices over the last year.

- 60%. The percentage of total, year-over-year CPI increase attributable to shelter costs.

The extras.

- One year ago today we didn't publish a newsletter, but we had just published our Friday edition, "Maybe all that military spending is a good thing."

- The most clicked link in Thursday's newsletter: The Biden administration's revamp of the organ transplant program.

- TikTok'ing: 56.1% of Tangle readers said the U.S. should not ban TikTok and 19.5% said they should. The rest were unsure or answered "other."

- Nothing to do with politics: Five planets (Mercury, Jupiter, Venus, Uranus and Mars) will align in the night sky near the moon this week, visible to most earthlings.

- Take the poll: What did you think of Friday's edition? Let us know.

Have a nice day.

A 90-year-old radiated tortoise named Mr. Pickles just became the father of three baby turtles. Mr. Pickles is the oldest animal at the Houston Zoo, and his partner Mrs. Pickles (53) just welcomed three new members of the family: Dill, Gherkin and Jalapeño. Mr. Pickles is the most "genetically valuable" radiated tortoise in the Association of Zoos and Aquariums' Species Survival Plan. His offspring bring hope for the critically endangered species, especially given how few offspring they have naturally. Plus, just look at them:

Did I pause to read a story about a 90-year-old turtle named Mr. Pickles who just became a first-time dad? Yes. Yes, I did. https://t.co/jHl7Z2UQEP

— Dana O'Neil (@DanaONeilWriter) March 23, 2023

Don't forget...

In order to spread the word about our work, we rely heavily on readers like you. Here are some ways to help us...

📣 Share Tangle on Twitter here, Facebook here, or LinkedIn here.

💵 If you like our newsletter, drop some love in our tip jar.

🎉 Want to reach 58,000+ people? Fill out this form to advertise with us.

😄 Share https://readtangle.com/give and every time someone signs up at that URL, we'll donate $1 to charity.

📫 Forward this to a friend and tell them to subscribe (hint: it's here).

🎧 Rather listen? Check out our podcast here.

🛍 Love clothes, stickers and mugs? Go to our merch store!

Member comments